Aging Economies — The Slow-Moving Challenge Reshaping Global Growth

Most economic crises arrive with some degree of surprise — a financial shock, a pandemic, a geopolitical rupture. Aging economies work differently. The demographic pressures now bearing down on developed nations have been visible for decades, charted in fertility data and actuarial tables, and discussed in policy circles since at least the 1990s. Yet effective responses remain elusive, partly because demographic change operates on a timeline that stretches far beyond any electoral cycle. The result is a slow-moving challenge that carries consequences as serious as any sudden crisis — just without the urgency that tends to force action.

A World Getting Older, Faster Than Expected

Rising Median Ages and Falling Birth Rates Are Redefining Developed Economies

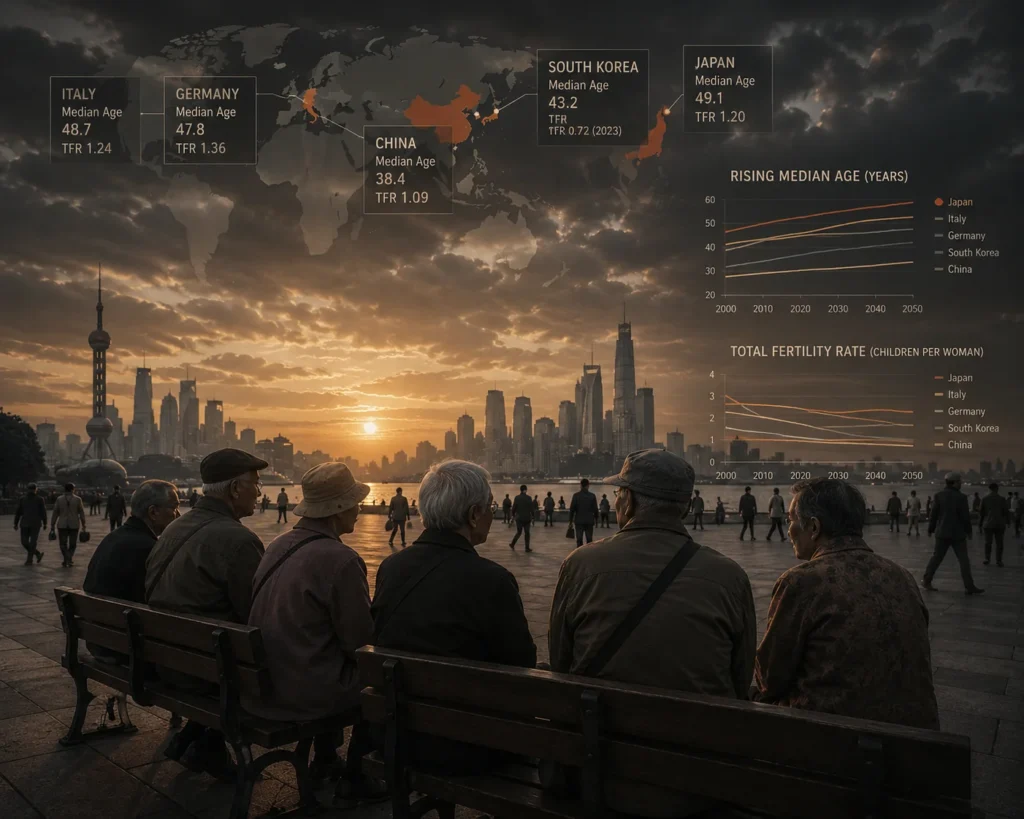

The numbers are striking. Japan’s median age now sits above 49. South Korea recorded a total fertility rate of just 0.72 in 2023 — the lowest ever measured for a developed country. Italy and Germany have had below-replacement birth rates for decades, while China, despite its size, is now projected to see its working-age population shrink significantly through the 2030s.

What makes this period distinct is not that aging is new, but that the pace and breadth of the shift are converging across multiple major economies at the same time. The post-World War II baby boom created an unusually large working-age cohort that sustained growth and funded generous social programs for decades. As that cohort moves into retirement, the structural support it provided is being withdrawn — and there is no comparable generation behind it in most developed nations.

When the Workforce Shrinks: The Economic Cost of Fewer Workers

A Contracting Labor Pool Doesn’t Just Slow Growth — It Reshapes It

A smaller workforce puts direct pressure on output. Fewer workers producing goods and services means lower potential GDP growth, all else being equal. But the effects go beyond headline growth figures. Labor shortages in sectors like construction, healthcare, and manufacturing are already visible in Germany, Japan, and South Korea, creating wage inflation in some areas while limiting capacity in others.

Productivity growth can offset some of this pressure — automation and artificial intelligence are often cited as partial solutions. That is plausible, but the transition is neither automatic nor immediate. Countries need capital investment, regulatory adaptation, and workforce retraining to capture those gains. For economies already managing fiscal strain from aging populations, funding that transition is a political as much as an economic problem.

The Fiscal Math of Aging: Healthcare and Pensions Under Strain

Rising Dependency Ratios Are Putting Pressure on Public Budgets

Every retiree supported by the pension system and public healthcare represents a fiscal commitment made years earlier, under different demographic assumptions. As the ratio of retirees to active workers rises — what economists call the dependency ratio — those commitments become harder to honor without raising taxes, cutting benefits, or borrowing more.

Japan is the clearest case study. Its public debt has climbed above 250 percent of GDP, driven in large part by social spending on an aging population. European nations face a less extreme but structurally similar trajectory. The IMF has repeatedly flagged pension and healthcare spending as long-term fiscal risks for advanced economies, and several countries have already moved to raise retirement ages or restructure benefit formulas — often against significant public resistance.

The political difficulty here is real. Retirees vote, and they vote in higher proportions than younger citizens. Reforms that reduce benefits or shift costs are disproportionately unpopular precisely among the demographic groups most likely to mobilize against them.

Aging Populations and the Question of Economic Dynamism

Demographic Shifts Can Influence Innovation, Risk-Taking, and Investment Patterns

There is an underexamined dimension to demographic aging that goes beyond labor supply: its effect on economic culture and risk appetite. Economies with older median populations tend to see lower rates of new business formation. Older workers are, statistically, less likely to start companies than those in their thirties. Consumer spending patterns also shift — away from durable goods, housing, and discretionary spending toward healthcare and services.

This does not mean older economies stop innovating. Japan retains genuine industrial strength. Germany still leads in engineering and manufacturing. But the composition of economic activity changes, and the sectors that drive long-term competitiveness — technology, venture-backed startups, high-growth industries — often flourish best in younger, more dynamic labor markets.

Immigration as a Demographic Lever: Useful, But Not a Complete Answer

Many Governments Are Turning to Migration to Offset Workforce Gaps

The most direct policy response to workforce shrinkage is immigration. Germany, Canada, and Australia have all recalibrated their immigration systems in recent years to attract working-age migrants, particularly in skilled and trades categories. The logic is straightforward: immigrants tend to arrive during their working years, contribute to tax revenues, and can partially offset the demographic gap.

The limits are equally clear. Immigration sufficient to fully compensate for low birth rates would require numbers that most societies find politically difficult to sustain. Integration outcomes vary. And migrants themselves age over time, deferring rather than resolving the underlying trend. Immigration is a useful tool, not a structural solution.

Demographics as a Component of National Competitiveness

Population Structure Increasingly Shapes Long-Term Economic Power

Countries with younger populations — parts of Sub-Saharan Africa, South and Southeast Asia, and portions of Latin America — carry a potential demographic dividend that aging economies no longer have. India surpassed China as the world’s most populous country in 2023, with a median age below 30. Nigeria is on a trajectory to become one of the world’s largest economies by mid-century, assuming governance challenges are addressed.

For developed nations, the demographic comparison matters in a direct way: a shrinking working-age population constrains tax revenue, limits military recruitment pools, and reduces the economic base from which governments project influence.

Aging as a Geopolitical Variable, Not Just an Economic One

Demographic trends are increasingly shaping which countries can sustain long-term strategic commitments. Military recruitment in Japan, South Korea, and several NATO members has become harder as the pool of eligible young men and women contracts. Defense spending as a share of GDP becomes more difficult to expand when competing fiscal demands from healthcare and pensions keep rising.

Aging economies represent one of the most predictable yet underestimated challenges facing developed nations. Governments have known about these trends for years. The forecasts have been accurate. What has been lacking is the political will — or the institutional capacity — to act on a timeline that does not align with election cycles. That gap between what is known and what is done may itself be the most consequential part of the story.