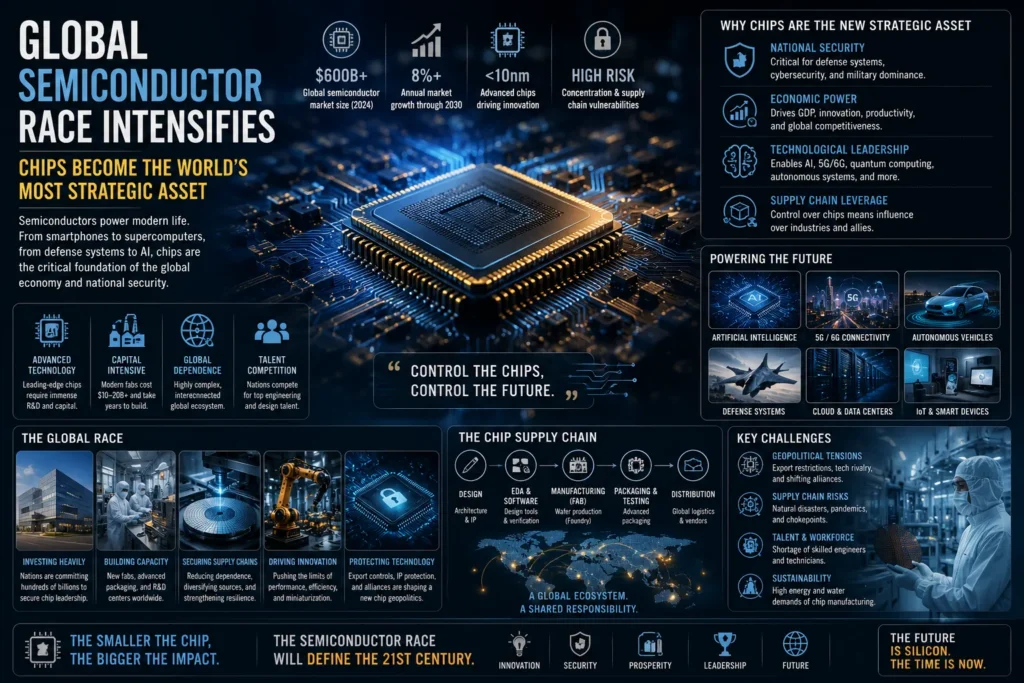

Global Semiconductor Race Intensifies — Chips Become the World’s Most Strategic Asset

The global semiconductor race intensifies as nations recognize that advanced chips have evolved far beyond mere industrial components to become the foundation of modern power projection. Countries that once viewed chip manufacturing as just another economic sector now treat semiconductor capacity as essential infrastructure, comparable to energy grids or military bases. This transformation reflects a stark reality: whoever controls advanced chip production holds disproportionate influence over artificial intelligence, defense systems, and the digital economy that underpins contemporary geopolitics.

Advanced Chips Drive National Security Infrastructure

Modern semiconductors power the core systems that define national security in the 21st century. Military drones, missile guidance systems, satellite communications, and cyber warfare capabilities all depend on specialized chips that operate under extreme conditions while processing vast amounts of data in real-time.

The Pentagon’s reliance on foreign-manufactured semiconductors has prompted significant concern among defense officials. Advanced fighter jets like the F-35 contain thousands of microprocessors, many sourced from global supply chains that include potential adversaries. This dependency creates vulnerabilities that extend beyond traditional military hardware into intelligence gathering, communications security, and strategic weapons systems.

AI and Defense Applications Accelerate Demand

Artificial intelligence applications in defense require cutting-edge processors capable of machine learning calculations at unprecedented speeds. These specialized chips enable autonomous weapon systems, predictive maintenance for military equipment, and sophisticated threat detection algorithms that form the backbone of modern defense strategies.

Nations Pour Billions Into Domestic Manufacturing

Government investment in semiconductor manufacturing has reached unprecedented levels as countries scramble to reduce foreign dependencies. The United States CHIPS and Science Act allocated $52 billion specifically for domestic chip production, while the European Union committed €43 billion through its European Chips Act by 2030.

China’s semiconductor ambitions remain the most aggressive, with estimates suggesting the country has invested over $100 billion in domestic chip development since 2014. These investments target everything from basic memory chips to advanced processors needed for artificial intelligence and quantum computing applications.

The scale of these commitments reflects a fundamental shift in how governments view semiconductor capacity. Rather than treating chip production as a market-driven industry, major powers now approach it as strategic infrastructure requiring direct state intervention and long-term planning.

Manufacturing Complexities Challenge Quick Solutions

Building advanced semiconductor facilities requires years of planning, specialized expertise, and supply chains that span multiple countries. Taiwan Semiconductor Manufacturing Company (TSMC) spent decades developing the institutional knowledge needed to produce the world’s most advanced chips. New facilities in Arizona and other locations face significant challenges replicating this expertise outside established manufacturing clusters.

Supply Chain Disruptions Expose Global Vulnerabilities

The semiconductor supply chain spans dozens of countries, creating multiple points of potential failure that can ripple through entire economies. Raw materials from Africa, manufacturing equipment from the Netherlands, assembly in Asia, and final integration in various locations create a web of interdependencies that no single country controls completely.

Recent disruptions have demonstrated how quickly chip shortages can impact industries far removed from technology. Automotive manufacturers faced production shutdowns when they couldn’t secure the processors needed for modern vehicles, while consumer electronics companies delayed product launches due to component shortages.

Geographic Concentration Increases Risk

Taiwan produces approximately 60% of the world’s semiconductors and over 90% of the most advanced chips. This concentration creates what analysts describe as a single point of failure for the global economy. Any disruption to Taiwan’s production capacity—whether from natural disasters, geopolitical tensions, or supply chain issues—could trigger worldwide economic consequences.

Technology Export Controls Reshape Market Dynamics

The Biden administration’s export controls on semiconductor technology to China represent the most significant trade restrictions in decades. These measures limit Chinese access to advanced chip-making equipment, software, and technical expertise needed to develop cutting-edge processors.

The controls specifically target chips capable of artificial intelligence and supercomputing applications, reflecting concerns that these technologies could enhance China’s military capabilities. Companies like NVIDIA must now obtain licenses to export their most advanced graphics processors to Chinese customers, fundamentally altering commercial relationships that took decades to develop.

European and Japanese companies face pressure to align with U.S. restrictions, creating tension between commercial interests and geopolitical alignments. Dutch company ASML, which produces the most advanced chip-making equipment, has limited sales to China despite significant revenue implications.

Asian Manufacturing Centers Maintain Dominance

Despite massive investment in domestic capacity, Asia continues to dominate global semiconductor production. Taiwan, South Korea, Japan, and China together account for over 75% of global chip manufacturing, a concentration that has proven difficult for other regions to challenge quickly.

South Korea’s Samsung and SK Hynix control significant portions of memory chip production, while Taiwan’s TSMC maintains leadership in advanced processor manufacturing. These companies have spent decades building the technical expertise, supplier relationships, and manufacturing infrastructure that competitors struggle to replicate.

Regional Specialization Creates Interdependencies

Different Asian countries have developed specialized roles within the semiconductor ecosystem. Taiwan focuses on contract manufacturing for global chip designers, South Korea dominates memory production, Japan supplies critical materials and equipment, and China handles assembly and testing for many products. This specialization creates efficiency but also interdependence that complicates efforts to relocate production.

AI Development Drives Unprecedented Chip Demand

The artificial intelligence boom has created insatiable demand for specialized processors capable of training and running large language models, image recognition systems, and autonomous vehicle software. Companies like OpenAI, Google, and Meta compete for access to the most advanced chips, often paying premium prices for priority access to limited supplies.

NVIDIA’s data center revenue exceeded $47 billion in fiscal 2024, driven primarily by demand for AI processors. This surge reflects how artificial intelligence applications require computational power that far exceeds traditional software, creating new categories of chip demand that didn’t exist five years ago.

The strategic implications extend beyond commercial applications. Nations view AI capabilities as essential for economic competitiveness, military advantage, and technological sovereignty. Access to advanced AI chips therefore becomes a matter of national priority rather than simple market dynamics.

Semiconductor Control Defines Emerging Global Order

In my view, the semiconductor race is becoming one of the defining competitions of this century. The countries that secure technological independence will shape the future global order. Unlike previous strategic resources such as oil or steel, semiconductors enable capabilities across multiple domains simultaneously—from economic productivity to military strength to technological innovation.

China’s pursuit of semiconductor self-sufficiency reflects recognition that chip dependency limits strategic autonomy. Similarly, U.S. efforts to maintain technological advantages through export controls demonstrate how semiconductor policy has become inseparable from broader geopolitical competition.

The outcome of this competition will likely determine which nations maintain influence over global technology standards, artificial intelligence development, and the digital infrastructure that increasingly defines economic and military power. Countries that fall behind in semiconductor capabilities may find themselves permanently dependent on others for the technologies that drive modern society.